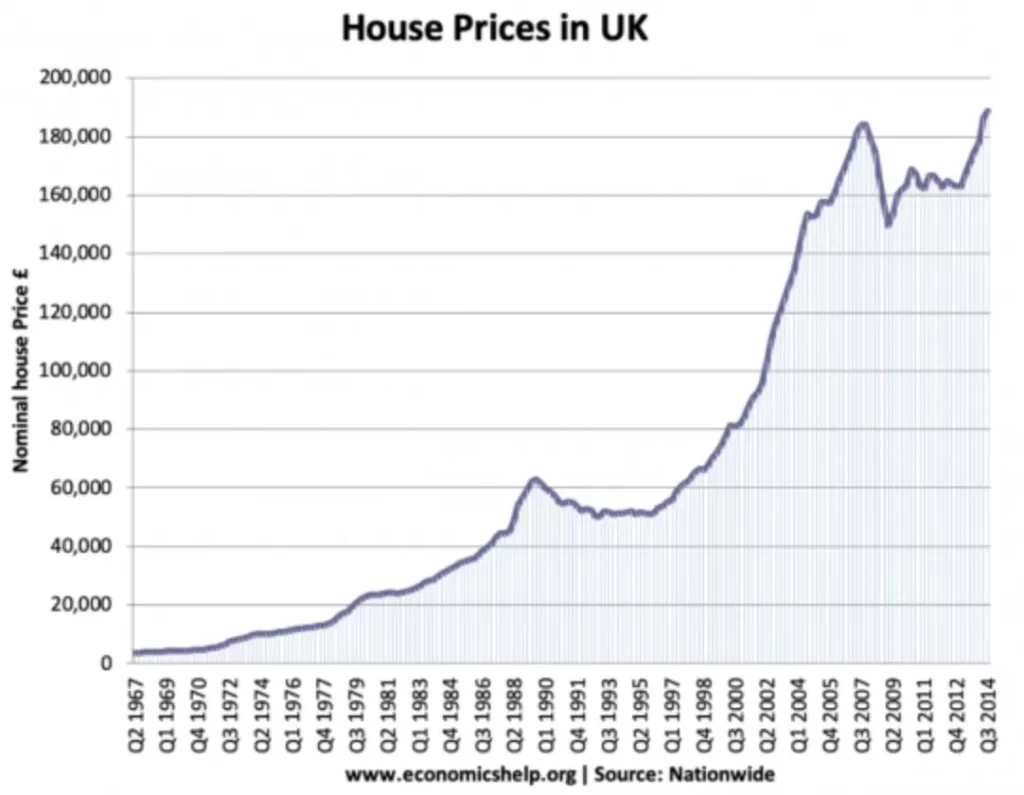

House Prices in the UK

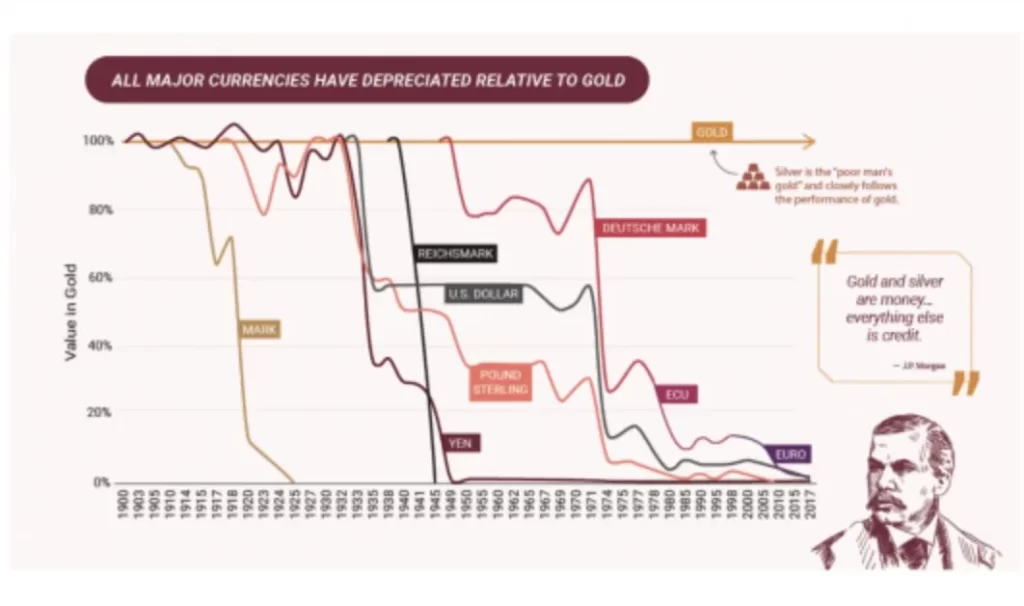

N.B. Richard Nixon took the American Dollar off the Gold Standard in 1971

So far, the music is still playing, and the musical chairs continue, but what happens when the music stops this time? Banks can be capricious, and they are well known for only giving you an umbrella when the sun is shining. What happens when their banks – the central banks have no umbrella to give them? Banks calling in loans are not unheard of and can be one of the most catastrophic things to happen to an individual or a business, especially if their whole life is built on them.

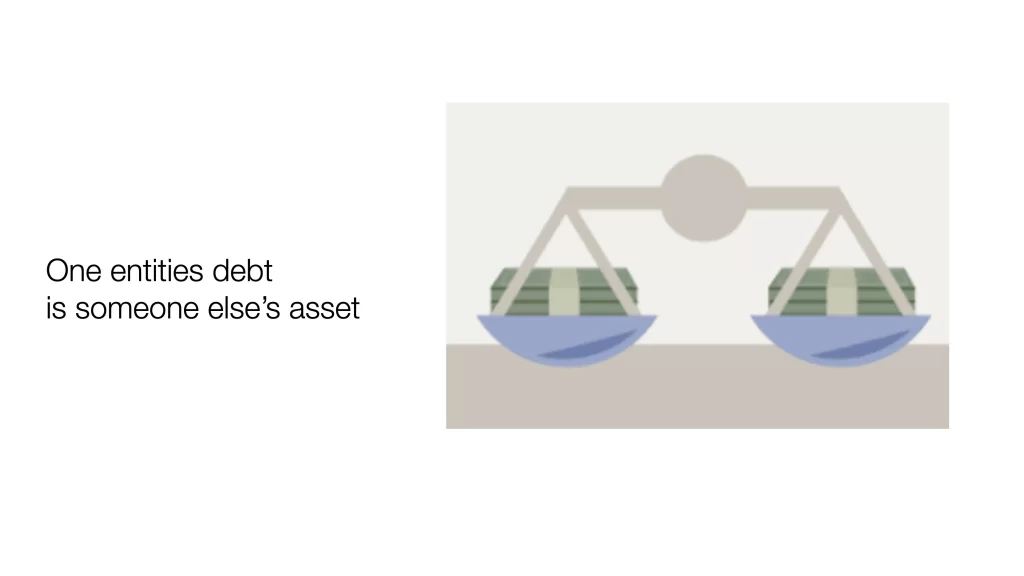

Debt became viable as a form of money once the banks convinced us that we should trust them to keep track of the value of money relative to the gold in their vaults. The argument for loosening the rules first occurred around World War I as the expenses for that adventure needed to be covered. So began the fudging of numbers, but hardly anyone still alive today remembers that discussion.

The paper debt, relative to gold, is now astronomical, but that means the paper assets are too – held in pension funds and promises to cover future welfare payments. The entire situation is incredibly finely balanced; it has to break at some point, it is mathematically inevitable – but what happens then?

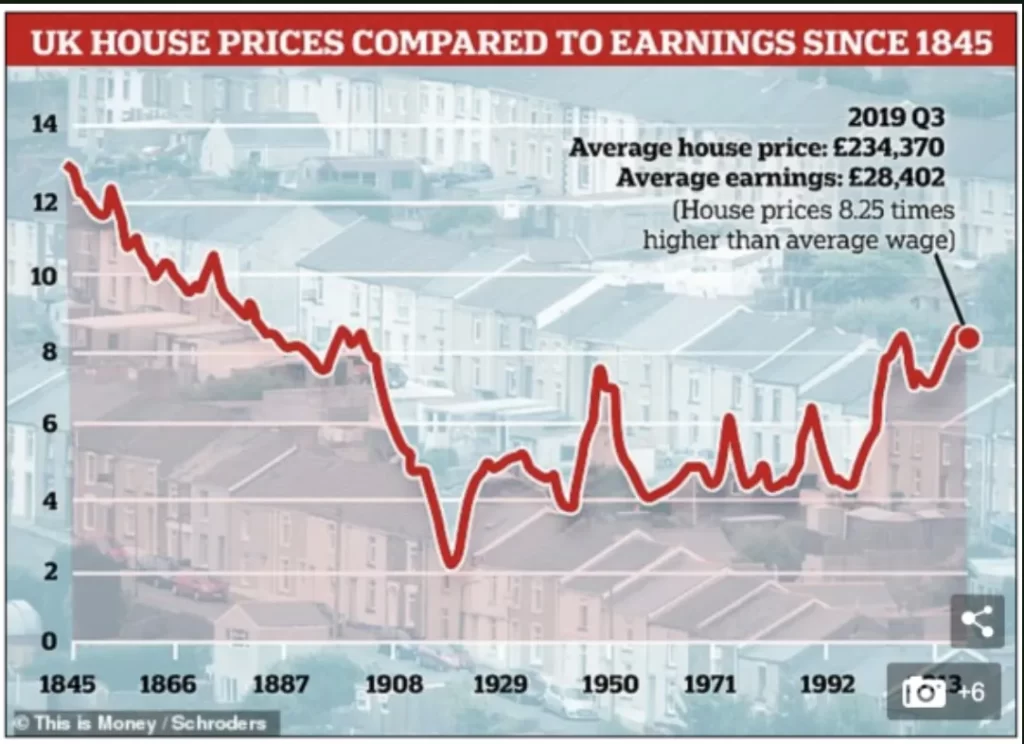

If you understand the benefits to society of sound money, this is a beautiful vision. But what about the assets that currently rely on debt? Most notably, our welfare systems, the industries that depend on the management of debt, i.e. the banks and the politicians, and finally, what about the value of Real Estate? Not only is property a massively over-leveraged asset, with a large proportion of the population and businesses committed to a mortgage, but what about those who only own it as an asset in their pension fund? Many of these properties remain empty for long periods, while the streets of some countries are filled with people who cannot live in a house at all?

If Bitcoin reaches its dream as a world reserve currency, this means the use of debt as a currency, as it is now, is ultimately obsolete. Yes, individuals and businesses will need some borrowing to help start a business or buy a home. Still, the obsolescence of debt as a form of currency means that its availability will be much more constrained than it was in the past, indicating a significant limitation to the growth of property prices going forward in the future.

At the moment, there are decentralised finance projects that are attempting to recreate a new financial system around cryptocurrency, including using debt-based models. Many of the organisers are still uncertain about how our economic future is likely to play out and hedge their bets as to which cryptocurrency to hitch their sail. This is hardly surprising given how currency has been managed for the duration of their lives. Who can blame them for believing that it is simply a popularity contest, and all they need to do is take an educated guess as to who the winner will be? After all, who knew that the American dollar was likely to emerge as the new financial powerhouse following the second world war?

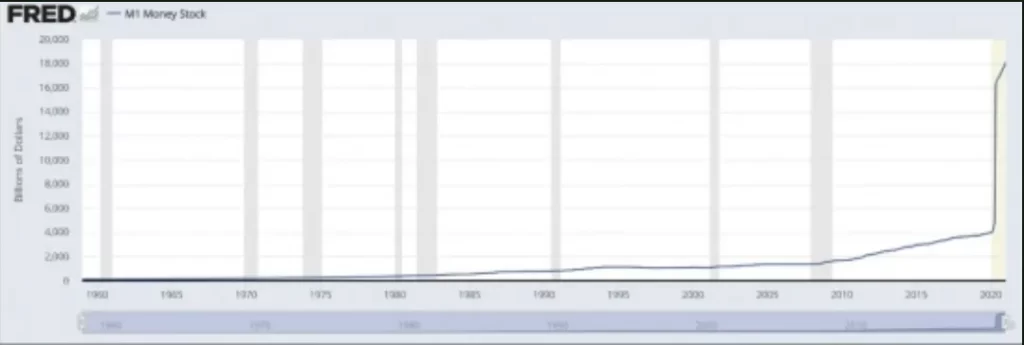

M1 Money Stock

So be wary of over-leveraged assets and don’t be deceived into believing that because Real Estate has exponentially increased in value over the last forty years, it is likely to continue. It is crucial to understand how the foundations of the financial system are actually built and if Bitcoin is the next currency, debt as a form of money will be obsolete.

We are at a unique point in history; we have been here before, but with different players. It is a melting pot of ideas and a simmering stew of possibilities for our money going forward. The actual direction, however, is apparent if you think about the issues deeply enough.

Bitcoin for Business

Watch my explanation of money, from the presentation I gave at Bitbrum, in Birmingham, in 2019.